When it comes to retirement planning, people often spend a lot of time thinking about the best way to increase their savings—but less time thinking about the best way to withdraw those savings when the time comes. This is unfortunate, because having an appropriate withdrawal strategy is a critical part of making sure those savings cover one's income and spending expectations.

Of course, everyone's situation is unique, and a retirement income strategy should embody such differences, but general principles still apply.

It starts with a budget that reflects your spending and income expectations. How much do you need? How much do you have? Then it's time to devise a strategy to make it work.

Use predictable income or cash to cover expenses

In retirement, you may not earn a paycheck from working, but you will still receive income from your investments, as well as Social Security, pension payments, annuities,1 and potentially other sources. On the other side of the ledger, some of your expenses will be for essentials like housing, car loans, food, and utilities, while others will be more discretionary "nice-to-haves" like vacations, charitable donations, or gifts to a grandchild.

We generally recommend covering essentials with predictable sources of income. Those include Social Security, pension payments, annuities, interest income from bonds, or the even cash or short-term bonds kept in reserve. (For most retirees, we suggest setting aside two to four years of essential expenses in cash or short-term bonds after accounting for other predictable income sources.)

Then, pay for any discretionary expenses by tapping growth assets or less predictable income sources from your portfolio. Stock dividends, distributions from mutual or exchange-traded funds, and proceeds from selling investments are often consistent, but not guaranteed, compared to Social Security or a bond coupon payment (barring a surprise default).

What's the advantage of this approach? In short, if you know an expense is coming due, you may not want to rely on volatile assets whose prices could drop right when you need to sell them. You'll end up having to sell more of them to raise a set amount of cash. And by selling more, you'll hobble your portfolio's ability to bounce back should the market recover later.

Generate cash flow when you rebalance

Periodically rebalancing your portfolio by selling assets that have risen in value while buying those that have lagged is a key part of maintaining a strategic asset allocation geared toward your goals and preferences. Retirees may also need to perform another kind of rebalancing by making their portfolios less aggressive as they age, usually by cutting back on more volatile assets, like stocks, in favor of less-volatile assets, like bonds.

But rebalancing isn't just about portfolio maintenance. It's also an opportunity to generate cash flow. Here's how that might work:

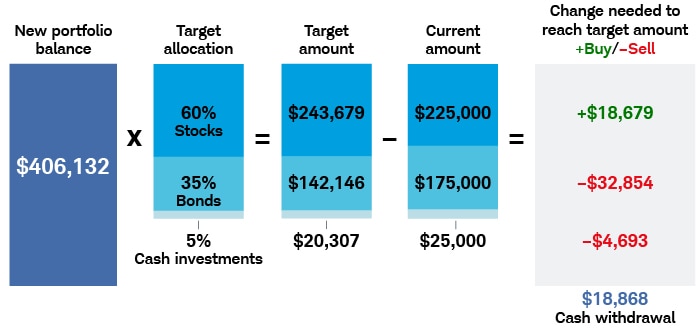

Consider this very simple hypothetical example: A 73-year-old investor with a $500,000 portfolio and a target allocation of 60% stocks, 35% bonds, and 5% cash investments. After a bad run in the market, the stock portion of his portfolio is down $75,000:

|

Starting portfolio (dollar value) |

Starting portfolio (percentage) |

Portfolio following market drop (dollar value) |

Portfolio following market drop (percentage) |

|

|---|---|---|---|---|

| Stocks | $300,000 | 60% | $225,000 | 53% |

| Bonds | $175,000 | 35% | $175,000 | 41% |

| Cash investments | $25,000 | 5% | $25,000 | 6% |

| Total | $500,000 | $425,000 |

At the same time, the investor needs to withdraw $18,868 from his investment portfolio. To figure out what to sell to meet his cash need, the investor should:

1. Subtract his cash need from his current portfolio balance:

Current portfolio balance: $425,000

Cash need: –$18,868

New portfolio balance: $406,132

2. Use his new portfolio balance and target allocation percentages to determine his target dollar amounts for stocks, bonds, and cash investments. As you can see, our hypothetical investor actually needs to buy more stocks—presumably at lower prices, which should work in his favor should the market turn around.

The example is hypothetical and provided for illustrative purposes only.

Be tax smart

What if you have to sell assets to cover your expenses? If you have savings spread across taxable brokerage accounts, tax-deferred accounts like individual retirement accounts (IRA) or a 401(k), and tax-free accounts such like a Roth IRA, you'll need to decide which accounts to tap first—and in what proportion. Here are some guidelines:

If you haven't yet reached age 73, when you must begin taking required minimum distributions (RMDs) from traditional IRA or 401(k) accounts, consider tapping your taxable brokerage accounts first. This will give your tax-deferred assets more time to grow until RMDs kick in, while you should consider leaving your Roth IRA assets untouched. These aren't subject to RMDs and could remain invested indefinitely during your lifetime.

First, part with investments that have lost value. Your losses can be used to offset any gains you may realize—a strategy known as tax-loss harvesting. And if you don't realize any capital gains, you can use those losses to offset up to $3,000 of your ordinary income per year until all your losses have been used up. Just be sure you don't violate the wash-sale rule by repurchasing the same or "substantially identical" securities within 30 days before or after the sale, lest your losses be disallowed.

Next, focus on selling investments you've held for more than a year to take advantage of lower long-term capital gains tax rates. You can sell these appreciated investments as part of your regular portfolio rebalancing, using whatever's necessary to meet your spending needs and reinvesting the remainder in underweight areas of your portfolio.

Possible exceptions would be if you didn't have enough assets in your taxable account to cover your cash needs, or if you had such significant tax-deferred savings that you were concerned about the tax hit that could come when your RMDs kick in at age 73. In either case, you may want to consider drawing down your tax-deferred accounts and your taxable savings at the same time.

With this approach, you take withdrawals from both your tax-deferred and taxable accounts in amounts proportionate to their balances. For example, imagine you had $800,000 in a traditional IRA and $200,000 in a brokerage account, for a total of $1 million in savings. If you required $50,000 from your portfolio to fund your spending, you'd take $40,000 (80%) from your tax-deferred IRA and $10,000 (20%) from your taxable brokerage account using the tax-efficient withdrawal strategy mentioned above. (Distributions from your tax-deferred accounts will be taxed as ordinary income, so the order in which you sell them doesn't matter from a tax perspective; however, you should still draw them down in a way that maintains your target asset allocation.)

Talk with your advisor or a tax professional to time your retirement income distributions wisely.

Funding your retirement with a strategic distribution plan

Keep these points in mind as you structure your retirement portfolio and create your own distribution plan, and be sure to watch for changes in your spending or income to ensure that your expectations are on track. In a prolonged down market, for example, you may want to curb or postpone discretionary spending to avoid drawing down your portfolio too quickly.

Creating income during retirement might sound daunting, but it doesn't have to be. Three steps—starting with a plan, investing in a balanced portfolio, and then distributing income from a variety of sources—can help you simplify the process and lay the groundwork for the kind of retirement you've always wanted.

1Annuity guarantees are subject to the financial strength and claims‐paying ability of the issuing insurance company.

We can help you with retirement income.

More from Charles Schwab

The Future of Social Security and Medicare?

The Most Important Ages of Retirement

5-Step Tax-Smart Retirement Income Plan

Related topics

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Diversification, asset allocation, and rebalancing strategies do not ensure a profit and do not protect against losses in declining markets. Rebalancing may cause investors to incur transaction costs and, when a nonretirement account is rebalanced, taxable events may be created that may affect your tax liability.

This information does not constitute and is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific advice is necessary or appropriate, Schwab recommends consultation with a qualified tax advisor, CPA, financial planner, or investment manager.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors.

Neither the tax-loss harvesting strategy, nor any discussion herein is intended as tax advice, it does not represent that any particular tax consequences will be obtained. Tax-loss harvesting involves certain risks including unintended tax implications. Investors should consult with their tax advisors and refer to Internal Revenue Service ("IRS") website at www.irs.gov about the consequences of tax-loss harvesting.

0523-3L6Z