An extreme downturn in the market can shake your confidence, but resisting the urge to flinch can pay off.

To demonstrate, we'll look at how three hypothetical investors—the Stalwart, the Reactor, and the Waffler—respond to the market over the course of 40 years.

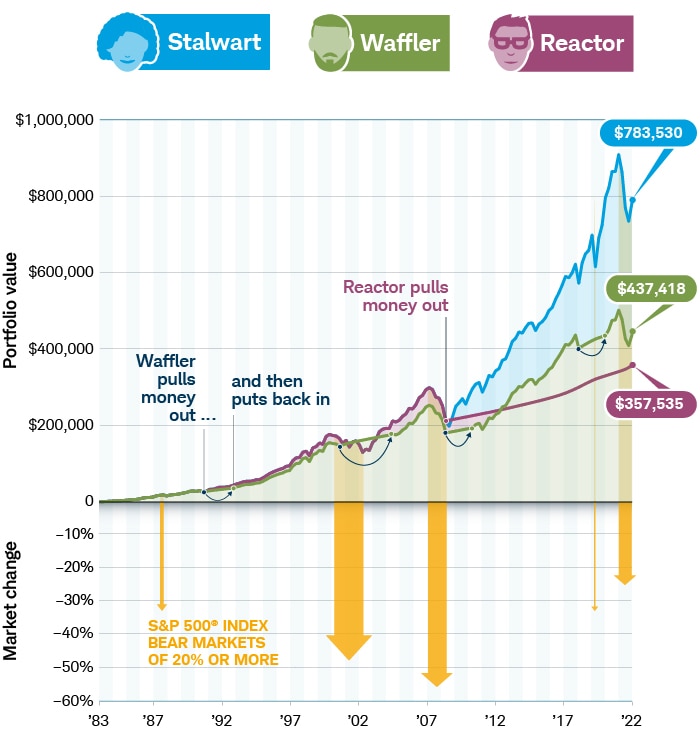

Same beginning, different endings

The Stalwart, the Reactor, and the Waffler all start in the same place: They begin their careers in 1983 at salaries of $18,580 and receive annual raises of 3%, as well as 10% promotion bumps every five years. By 2022, they're making $112,560 a year.

They start investing at age 26, saving 10% of their annual salaries. Initially, they're all aggressive—with portfolios comprising 50% large-cap stocks, 25% international stocks, 20% small-cap stocks, 5% cash—and then shift into increasingly conservative allocations over time.

Forty years later, despite their shared origin stories, our investors' portfolios differ in size by hundreds of thousands of dollars. Why? As we'll see below, how they reacted to bad markets pretty much determined their destiny. (Spoiler alert: The person who reacted the least ended up gaining the most.)

Wealth accumulated, 1983–2022

Source: Schwab Center for Financial Research with data provided by Morningstar, Inc.

The example is hypothetical and provided for illustrative purposes only. The asset allocation plan performance is the weighted averages of the performances of the indexes used to represent each asset class in the plans, and the plans are rebalanced annually. Fees and expenses would lower returns. Using the same methodology, had a saver stayed invested over four decades in a fund that tracks the S&P 500® index, which is all equities, they would have experienced greater volatility and had an ending wealth of $1.46 million. However, a portfolio comprised 100% equities is not in conjunction with our point of view, which is a diversified portfolio.

The Stalwart

This disciplined investor sat tight and continued to invest, no matter how the market performed. The Stalwart shifted to a moderately aggressive portfolio (45% large-cap stocks, 20% international stocks, 15% small-cap stocks, 15% bonds, 5% cash) at age 39 and then moved to a moderate allocation (35% large-cap stocks, 15% international stocks, 10% small-cap stocks, 35% bonds, 5% cash) at age 52. As retirement neared, the Stalwart's portfolio had grown to more than $783,530.

The Waffler

The Waffler followed the same allocation plan as the Stalwart, but this wary investor moved almost all his money out of the market after every year of losses. However, he didn't completely withdraw: He continued to put 10% of his salary in 3-month Treasury bills whenever he was out of the market.

Then, if the market was up after two years, the Waffler reinvested in a portfolio suitable for his age. This strategy resulted in an ending balance of $437,418, cutting his potential growth by more than 44%.

The Reactor

This investor stuck it out through a brief bear market in the late '80s as well as the early 2000s recession. Then, midway to the Reactor's retirement, the 2008 financial crisis hit. He pulled all his money out of the market—and kept it out.

He continued to put 10% of his salary in 3-month Treasury bills with hopes of recouping some of his losses. But at the end of 40 years, he only managed to save $357,535, cutting his potential earnings by almost 55%.

Bottom line

Bad markets can definitely cause big feelings, but it's generally not a great idea to let emotions take control of your portfolio.

A better approach would be to make a plan you can stick to no matter what the market's doing. You can absolutely modify those plans as your goals or situation change, but such adjustments should occur without the influence of any temporary gut feelings. Otherwise, the consequences could be with you for life.

We can help you manage your portfolio.

More from Charles Schwab

Stocks Extend November Gains Ahead of Holiday

Opening Market Update

Closing Market Update

Related topics

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Indexes used for model asset allocation plans: U.S. large-cap stocks: S&P 500® Index. U.S. small-cap stocks: Russell 2000® Index; the CRSP 6-8 was used prior to 1979. International stocks: MSCI EAFE® Net of Taxes. Bonds: Bloomberg Barclays U.S. Aggregate Bond Index; the Ibbotson Intermediate-Term Government Bond Index was used prior to 1976. Cash equivalents: FTSE 3-Month U.S. Treasury Bill Index; the Ibbotson U.S. 30-day Treasury Bill Index was used prior to 1978.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

Diversification, asset allocation, and rebalancing strategies do not ensure a profit and cannot protect against losses in a declining market. Rebalancing may cause investors to incur transaction costs, and when a non-retirement account is rebalanced, taxable events may be created that may affect your tax liability.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Investing involves risk including loss of principal.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

0423-3FB1