Option traders know there are two ways for an options position to profit:

- When a long option goes up in value

- When a short option goes down in value

If the option moves in the opposite direction, the position loses money. The same is true of spreads, which are made up of more than one leg, but option traders must look at the net value of the trade.

However, don't confuse the net value of an options position with what you want the underlying stock to do. For instance, if you're short a put, you likely want one of two things to happen. You might want the stock price to go down in hopes of getting assigned on the short put and purchasing the stock at a lower price (at the strike price of the put). Or you likely want the underlying to go up, which should lower the value of your put. Then you either buy the put back at a lower price or let it expire worthless.

What exactly is it, then, that makes options prices (and thus spreads) go up or down in value? The short answer: Follow the options greeks.

The options greeks are risk metrics that help quantify the relationship between an underlying stock and its options prices. Delta and gamma relate to the price changes in an options contract to the movement of the underlying stock price. Vega relates to changes in the price of an option due to changes in implied volatility, which is the market's perception of the future volatility of the underlying security directly reflected in the option premium. Implied volatility is forward-looking, changing often, and expressed as an annualized number as a percentage (such as 25%). And then there's theta.

What is theta, or time, decay?

Theta measures the inevitable loss in value that options experience as time passes. Of all the options risk measures, the passage of time is the one thing that's certain. Time marches on, which means that most options, which have fixed lifespans defined by their expirations, will continue to "decay," or lose value over time. And if an option is going to lose value over time, it's sometimes possible to profit from that option by shorting it.

Note that the other greeks play a part in how options prices change, but we'll assume everything remains the same for the purposes of this article.

If you buy an option, your theta value is negative. Theta decay is one of the (few) consistencies that option traders can rely on. Long options lose value over time and as they near their expiration date, all else equal, the rate of theta decay accelerates the closer you get to contract expiration. However, if you're short an option, time is on your side (so to speak) because your theta value is positive.

Extrinsic value and the dynamics of options theta

How much is an option expected to lose daily due to time decay? Check theta. For example, if a stock is trading for $215 and the 215-strike call options have .10 thetas, then that options contract would decay approximately $0.10 per day. The 230-strike call, which is out of the money (OTM) by $15, has a theoretical decay of only $0.06 per day. That makes sense because the further OTM the option is, the less value there is to decay.

But theta isn't just about price. That is, an in-the-money (ITM) option won't have a higher theta than an at-the-money (ATM) option despite having a higher price. Why? The value of an option is broken down into two components: intrinsic value and extrinsic value. Intrinsic value is the difference between the stock price and strike price of an ITM option. It's also the amount the option would be worth if it were exercised today. Extrinsic value is the difference between the options premium and the intrinsic value.

At expiration, an option has no extrinsic value. It's either ITM by an amount equal to its intrinsic value, or it's worth zero and expires worthless. That's why many option traders refer to extrinsic value as its "time value" or "time premium."

Looking for theta-based options strategies? Here are 3 to consider

Some options strategies seek to take advantage of the passage of time. Each has its own objectives—and its own set of risks. Make sure you understand them before jumping in.

Here's the setup: Recall from above that time decay isn't the same for every strike. ATM options have the highest rate of decay (all else equal). As options move either OTM or ITM, the rate of decay drops and approaches zero. Also, shorter-term options decay faster than longer-term options (again, all else equal). This rate of decay speeds up as an option gets closer to expiration.

It's these two facets that options traders put to work when seeking to profit from the following strategies.

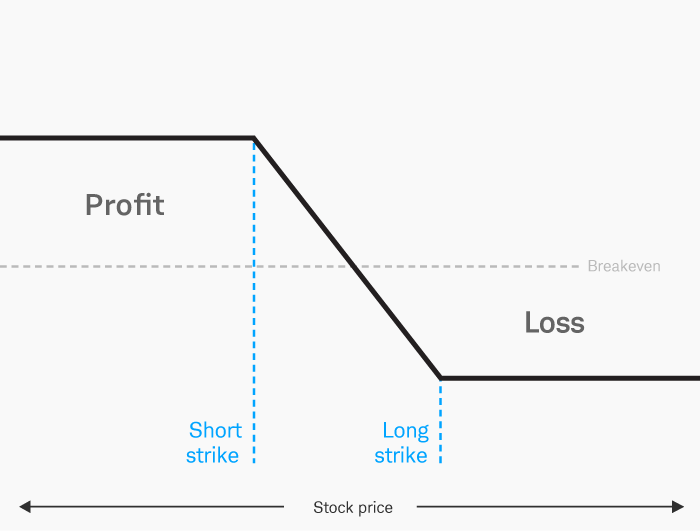

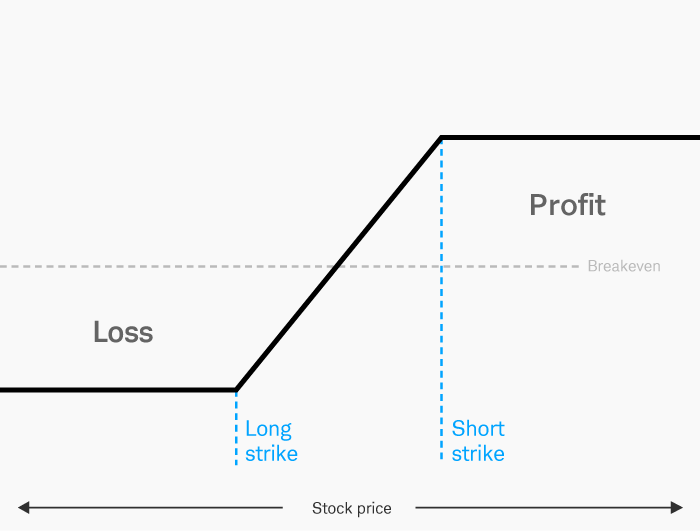

Strategy #1: Short OTM vertical spread

A short vertical spread involves selling an option that's ATM or slightly OTM and buying an option that's further OTM. A call vertical spread is made up of two call options; a put vertical is made up of two put options. Vertical spreads have a directional bias in the underlying stock—a short call vertical is bearish, and a short put vertical is bullish.

Short call vertical

Note the points of maximum profit and maximum loss to see the directional bias. For illustrative purposes only.

Short put vertical

Note the points of maximum profit and maximum loss to see the directional bias. For illustrative purposes only.

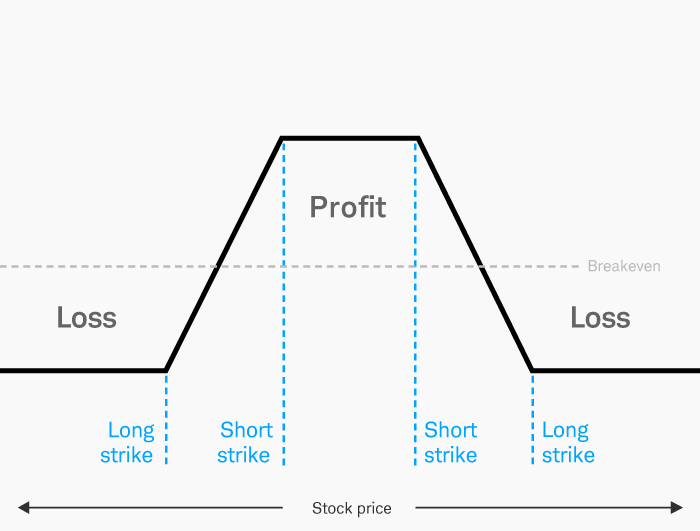

Strategy #2: Iron condor

An iron condor is a four-leg spread made up of a short OTM call vertical spread and a short OTM put vertical spread in the same expiration cycle. Typically, both vertical spreads are OTM and centered around the current price of the underlying. Similar to a single vertical spread, the risk is determined by the distance between the strikes of the vertical.

But unlike the vertical spreads themselves, the directional bias of an iron condor is neutral.

Iron condor

Note the points of maximum profit and maximum loss to see the neutral bias. For illustrative purposes only.

In the iron condor's best-case scenario, the price of the underlying will stay between the two short strikes through expiration, and both vertical spreads will expire worthless. The maximum loss would occur if the stock moved outside the long strikes of the short call or short put spreads. That loss would be the distance between the strikes of the vertical spread minus the credit received from the sale of the iron condor. Any transaction fees subtract from profits and add to losses.

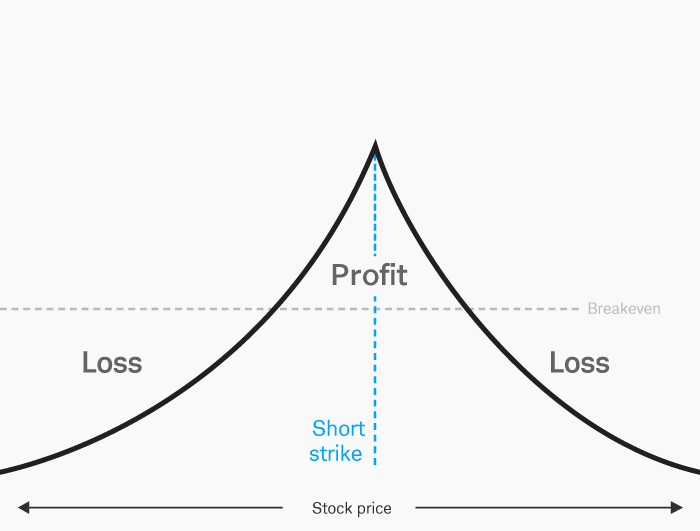

Strategy #3: Calendar spread

Note that when trading vertical spreads and iron condors, the strikes are all within the same expiration cycle. They target the points of maximum theta within a cycle by placing the short strikes closer to ATM than the long strikes. Calendar spreads, however, target the "other rule of theta"—theta tends to accelerate as you approach expiration.

A calendar spread involves the sale of an option (a call or put) with a near-term expiration date and the purchase of the same option type and strike price but with a later-dated expiration date. It's a defined-risk strategy, with the risk typically limited to the amount you paid for the spread, or the debit. The best-case scenario is for the underlying to be right at the strike price when the short option expires (or the near-term expiration date; see figure below). The worst-case scenario would be realized if the underlying stock moved far enough away from the strike price of the options when the short-term option expires. Here, the loss would be the debit paid for the calendar spread plus any transaction fees.

Calendar spread

Note the points of maximum profit and maximum loss to see the neutral bias. For illustrative purposes only.

When trading calendar spreads, you must carefully manage the trade as the expiration date of the near-term option approaches. While short options can be assigned at any time, they're more likely to be assigned if they're ITM or close to being ITM. If the short options expire (whether ITM or OTM), the later-dated option lingers on. Then the calendar spread becomes a long single-leg option after the short option expires.

Many option traders opt to liquidate or roll a calendar spread at least a few days before the first expiration date. However, keep in mind that closing or rolling the position will entail additional transaction fees, which may affect any potential return. In the case of the short option being assigned at or before expiration, the resulting position would be the later-dated option plus long or short 100 shares of the underlying stock (it rarely makes sense to exercise the long option to cover assignment on the short option because the long option likely still has time value, which is lost if the option is exercised). Assignment of the short option could significantly change the delta exposure of the original calendar spread and require additional trade management.

Bottom line on options theta and decay strategies

Although each of these strategies involves long options that experience their own time decay, if the trade goes as planned, the short options bring in more than the long options lose to net out a profit. But if there's an adverse move in the underlying, like when a short OTM vertical spread moves ITM, the trade's net time decay can work against you. Or in the case of a calendar spread, if the implied volatility of the front leg were to rise relative to the volatility in the later-dated leg (all else equal), the spread price would go against you.

A strategy that seeks to profit from the inevitable options decay is one way for option traders to put time on their side and potentially have it work in their favor. However, keep in mind, these are advanced options strategies that require a good understanding of the risks and the active trade management involved.

Just getting started with options?

More from Charles Schwab

Looking to the Futures

Today's Options Market Update

The Truth About Corporate Stock Earnings Estimates

Related topics

Options carry a high level of risk and are not suitable for all investors. Certain requirements must be met to trade options through Schwab. Please read the options disclosure document titled Characteristics and Risks of Standardized Options. Supporting documentation for any claims or statistical information is available upon request.

Spread trading must be done in a margin account. Multiple leg options strategies will involve multiple per-contract charges.

Commissions, taxes, and transaction costs are not included in this discussion but can affect final outcome and should be considered. Please contact a tax advisor for the tax implications involved in these strategies.

Short options can be assigned at any time up to expiration regardless of the in-the-money amount.

With long options, investors may lose 100% of funds invested.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

0223-2GZN