Long valued as a tax-smart way to pay for a child's college education, 529 plans have another, less obvious use: multigenerational education planning.

Unlike most other tax-advantaged savings accounts, 529 plans don't have annual contribution limits. Instead, they have total contribution limits set by the state in which they're administered, ranging from $235,000 in Georgia and Mississippi to $553,098 in New Hampshire. Better yet, even if the total contribution limit is reached, there's no law that limits how large the account can grow over time or how long it can remain open.

"Given the high contribution limits and unrestricted growth potential, it's easy to see how a well-funded 529 account could cover education costs for generations—provided your plan permits it," says Austin Jarvis, director of estate, trust, and high-net-worth tax at the Schwab Center for Financial Research.

For this strategy to work, your plan must allow you to both change the beneficiary and name a successor account owner so that unused funds can be tapped by future generations. "If your plan doesn't permit both, you may want to shop around for one that does," Austin says. "You're free to choose a plan administered in any state, though you may not be able to deduct contributions to an out-of-state plan from your state taxes."1

In 2023, individuals can contribute up to $17,000 per year and couples up to $34,000 per year without eating into their lifetime gift and estate tax exemption (for 2023, $12.92 million for individuals and $25.84 million for married couples). However, if you want to supercharge your 529's growth potential, you can contribute five years' worth of gifts in a single year—$85,000 for an individual and $170,000 for a couple—so long as you treat those gifts as occurring over five successive tax years.

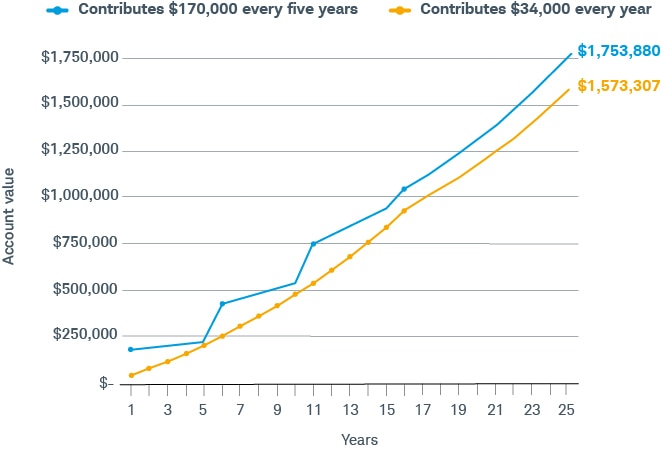

Supercharge your savings

Thanks to compound growth, a couple who frontloads a 529 account with $170,000 every five years (until they reach a total contribution limit of $550,000) would end up with nearly $200,000 more after 25 years than if they had contributed $34,000 per year—even though the total contribution amounts are identical.

This chart is hypothetical and for illustrative purposes only, and not intended to be reflective of results you can expect to achieve. Example assumes 6% annual returns and does not reflect the effects of fees. Maximum contributions based on 2023 gift tax exclusion limits.

Finally, be aware that this strategy may not be available in the future. "Some lawmakers view it as a tax loophole that should be closed," Austin cautions. "If the laws do change, an estate could be forced to liquidate the account upon the owner's passing, which could create estate-tax consequences."

1Thirty-six states and the District of Columbia offer tax credits or deductions for contributions to their state-sponsored 529 plans, and nine of those states offer a state income tax benefit for contributions to any 529 plan.

Discover more from Onward

Keep reading the latest issue online or view the print edition.

Learn more about saving for college.

More from Charles Schwab

AI Voice Cloning: The Newest Cyber Scam

5 Ways to Use Annuities in Your Estate Plan

Celebrating 50 Years of Innovation

Related topics

Before investing, carefully consider the plan's investment objectives, risks, charges, and expenses. This information and more about the plans can be found in the Schwab 529 Education Savings Plan Guide and Participation Agreement available from Charles Schwab & Co., Inc., and should be read carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Investors should consider, before investing, whether the investor's or designated beneficiary's home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available in such state's qualified tuition program.

This information does not constitute and is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific advice is necessary or appropriate, Schwab recommends consultation with a qualified tax advisor, CPA, financial planner, or investment manager.

0823-34E5