When establishing your portfolio's asset mix, it's important to consider your risk tolerance, or the degree to which you can emotionally endure losses. But there's another side to the coin: risk capacity.

"Risk tolerance is a state of mind and can fluctuate wildly in response to the market," says Susan Hirshman, director of wealth management at Schwab Wealth Advisory, Inc. "Risk capacity, on the other hand, is fixed: Your goals have an end date, and you either have time to bounce back from losses or you don't."

When your risk capacity and risk tolerance don't align, it creates challenges—especially as your time frame shrinks. Susan points to two such scenarios:

- When the market is struggling and portfolio values are dropping quickly, investors with a low risk capacity might be tempted to cut back on their stock exposure or cash out entirely in an attempt to soften the blow. "But selling in a downturn just means locking in those losses and potentially missing out on the rebound, making it that much harder to recover your lost funds," Susan says (see "Staying the course").

- When the market is on fire, on the other hand, investors tend to take on more risk than is prudent. "Feeling like you're missing out on gains can lead you to increase your exposure to higher-risk, higher-reward investments," Susan says. "But if you're nearing your goal, you should focus on preserving what you've saved rather than risking it for the prospect of a few extra percentage points."

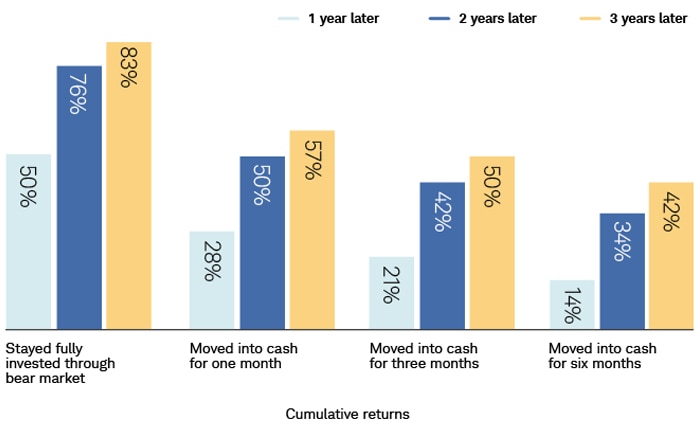

Staying the course

Cashing out during a downturn may curtail some losses—but it's also likely to undercut gains as the market recovers. And the longer you sit on the sidelines, the farther behind you'll fall.

Source: Schwab Center for Financial Research and Morningstar.

Data analyzes the five periods from 10/1974 through 03/2022 during which the S&P 500® Index fell by 20% or more. Market returns are represented by the S&P 500 Total Return Index, and cash returns are represented by the total returns of the Ibbotson U.S. 30-Day Treasury Bill Index. Cumulative returns are calculated using the simple average of returns from each period and scenario. Past performance is no guarantee of future results.

Your risk capacity, not your risk tolerance, should drive your investment decisions. But determining whether your portfolio aligns with your goals isn't always straightforward. For example, you may have a retirement date in mind, but that doesn't mean you need access to all your savings on that date.

"Generally speaking, you should have two to four years' worth of expenses in stable, relatively liquid investments, but the rest of your portfolio can be invested for long-term growth," Susan says. "In that way, your overall capacity for risk might actually be higher than you assume."

When in doubt, Susan suggests working with an advisor who can help ensure the risk in your portfolio aligns with your capacity to weather a downturn.

We can help you manage your portfolio.

More from Charles Schwab

How Well Do You Know Market Cap?

Celebrating 50 Years of Innovation

4 of Investors' Biggest Concerns Now

Related topics

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Investing involves risk, including loss of principal.

1122-2ZAT